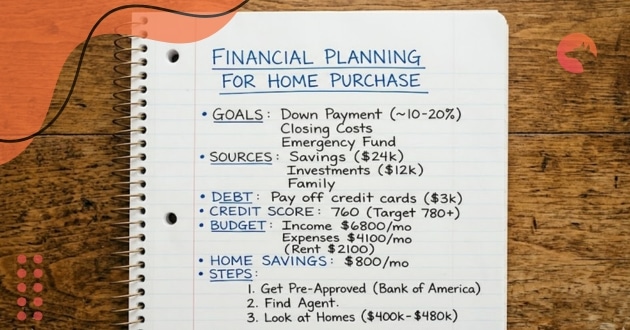

Financial planning for home purchase is the fundamental starting point for achieving homeownership in the real estate market.

Furthermore, this year is defined by experts as the Great Housing Reset, a period of stabilization where extreme volatility gave way to a necessary technical normality.

Understanding financial planning for home purchase allows the buyer to navigate safely among interest rates that fluctuate between 5.50% and 6.3%. For this reason, the prospective analysis of Treasury yields becomes a central piece in the purchase decision.

This article presents the pillars of financial planning for home purchase with the purpose of ensuring that your acquisition is a wealth-generating asset. You will find details about everything you need to conquer your home.

Winning Strategies for Financial planning for home purchase

Financial planning for the purchase of a property involves various approaches, adjusted to the buyer’s liquidity profile and long-term objectives. Let’s look at the main strategies.

1. Strategic Capital Allocation (Financial Leverage)

- Reduced Down Payments: Today, the traditional practice of a 20% down payment has been made more flexible. This is especially true for buyers with excellent credit history. Many opt for down payments of only 3% to 5% on conventional loans.

- Liquidity Advantage: The remaining capital is kept invested in markets with yields superior to the cost of Private Mortgage Insurance (PMI).

- Analysis Requirement: This leveraging technique demands rigorous financial planning. It involves comparing the cost of PMI with the real return of the investment portfolio. This maintains liquidity as a safeguard in moderate interest rate scenarios.

2. Government Affordability Strategies (Financial Planning For Home Purchase)

Government initiatives, such as FHA and VA, are fundamental in assisting first-time buyers and veterans.

- FHA (Federal Housing Administration): Allows reduced down payments for applicants with credit scores starting at 580.

- VA (Veterans Affairs): Offers the most efficient form of leverage, with the possibility of 0% down payment.

- USDA (United States Department of Agriculture): In 2026, it gained prominence in expanding suburban areas, providing full financing for properties in specific geographical zones of low population density.

The decision between these modalities should be based on a technical analysis of the mortgage insurance cost and the intention of long-term permanence in the property.

Quick Comparison of Financing Modalities

Below, we present a comparative analysis of the main credit modalities available in the current market. This facilitates the decision within your financial planning for home purchase.

Note that differences in rates and requirements can alter the total cost of the property by hundreds of thousands of dollars over the 30-year contract.

| Feature | Conventional Loan | FHA Loan | VA Loan | USDA Loan |

| Minimum Credit Score | 620 | 500-580 | Generally 580+ | 640 |

| Minimum Down Payment | 3% to 5% | 3.5% | 0% | 0% |

| Mortgage Insurance | PMI (Cancelable) | MIP (Lifetime) | None | Annual Fee |

| Property Use | Primary or Inv. | Primary Only | Primary Only | Qualified Rural |

| Loan Limit | $832,750+ | Regional | No fixed limit | Based on Income |

AI Technology That Will Help You with Financial Planning

AI revolutionizes real estate financial planning. Modern tools simulate complex scenarios with precision, surpassing manual spreadsheets by including variables such as inflation and taxes.

Algorithms predict neighborhood appreciation trends (based on infrastructure and construction data), optimizing the return on invested capital.

Thus, using AI is essential for high-performance transactions.

1. Origin Platform (Financial Planning For Home Purchase)

The Origin platform is the standard for a holistic view of real estate finances.

It connects accounts and uses AI to simulate the impact of a real estate purchase on retirement (20-30 years), making it ideal for prospective modeling in financial planning for home purchase.

It suggests automatic adjustments to the portfolio to generate the necessary down payment capital on the desired date, considering fluctuations and projected inflation.

2. YNAB Method

YNAB manages daily cash flow and the psychology of spending, allowing for a “stress test” for the future mortgage.

By saving the difference between the current rent and the expected installment, the buyer validates the sustainability of the plan and accumulates the down payment.

This creates the necessary financial muscle memory post-purchase. The software also identifies superfluous expenses, whose elimination can anticipate the purchase.

3. Credit Karma and Monarch (Financial Planning For Home Purchase)

Credit Karma is essential for monitoring and optimizing your credit score in real-time, suggesting quick-impact actions such as paying balances on strategic dates.

Monarch Money, on the other hand, focuses on collaboration between couples, unifying incomes and expenses on a single visual dashboard.

Both are fundamental for maintaining the transparency and discipline necessary in a shared financial planning for home purchase.

Moreover, the synchronization of banking data is instantaneous, allowing the couple to make decisions about extraordinary expenses without compromising the home reserve fund.

Frequently Asked Questions About Financial Planning For Home Purchase

1. What is the percentage of income allocated to housing in 2026?

The total cost of housing should ideally be less than 28% of gross monthly income.

A conservative financial planning approach, unlike higher rates allowed by some banks, guarantees a margin for investments like 401k.

This safety margin distinguishes the prosperous homeowner and allows for diversification in times of moderate inflation.

2. Is it worth waiting for interest rates to drop further?

Trying to guess the market bottom is risky. If rates fall, prices can rise quickly due to pent-up demand.

The strategy is to buy the right property when the installment is affordable today, using refinancing to optimize costs if the scenario improves.

3. How to deal with hidden costs of purchasing? (Financial Planning For Home Purchase)

Closing costs, inspection fees, and annual increases in association fees (HOA) and taxes are common surprises.

Include a 10% safety margin in your financial planning for unforeseen circumstances and variations. This ensures that the dream of homeownership does not become a financial problem.

4. Are down payment assistance programs safe?

Yes, many Down Payment Assistance Programs (DPA) have state agency support and offer funds that can be forgiven. This is provided you reside in the property for a specific period.

However, it is crucial to verify if this advantage does not result in a penalty on the interest rate of your main loan.

Furthermore, the technical analysis of financial planning for home purchase compares the immediate capital gain with the total cost of interest over time. This ensures that the initial help does not end up costing more in the long run.

Conclusion

Financial planning for home purchase in 2026 requires technical precision and economic maturity to navigate the Great Housing Reset.

We covered everything from credit shielding and the PITI rule to the use of AI and new laws that favor the individual buyer.

The acquisition of a property remains the basis for building generational wealth, but the rules of the game have changed to prioritize mathematical efficiency over speculation.

Start your credit audit now and use the recommended tools to structure your plan. The market rewards preparation, so take the first step towards your home today.

A fundamental tip is that, if you are a couple, you should organize your finances well, after all, you will be making a commitment for life. Therefore, we recommend that you apply the main personal finance tips for couples starting today.